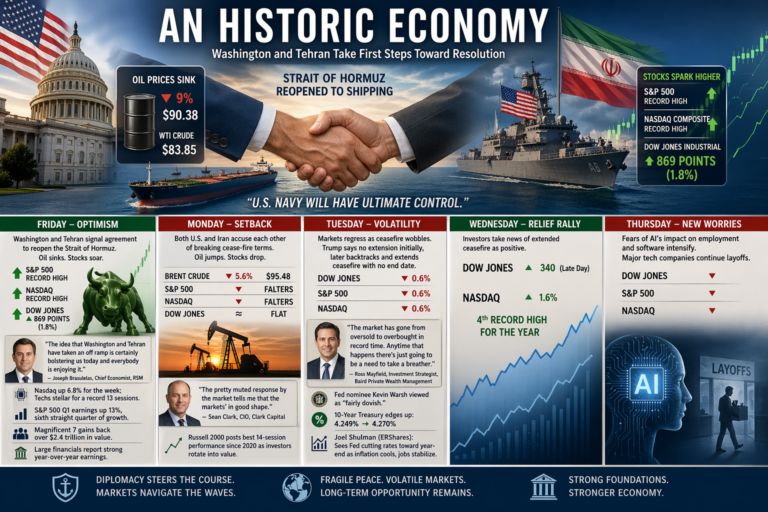

After dealing with tariff announcements, threats and start dates for several months, the market finished the week near where it all started. Friday the indexes slipped reacting to President Trump’s proposed 35% tariff on Canadian goods, upping it from 25% to 35%. Backing up to Wednesday night, the president punished Brazilian goods with a stiff 50% tariff. All tariff implementation is set (required by President Trump) for August 1st, if no trade agreement is reached beforehand. After all the weeks of tariff rhetoric, thick-skinned investors and traders have managed to ‘shake-off major collateral damage.’ Another non-issure appears to be inflation and the direction thereof. As tariffs kick in and product pricing increases inflation numbers that potentially go up, seemingly are not yet ‘dialed in’, a near non issue with many investors. “We are all waiting for the ultimate impact of what this is actively going to be once the tariffs are enacted,” said Allen Bond, managing director at Jensen Investment Management. For the week the Dow Jones Industrial Average and S&P 500 slid 1% and 0.3% respectively, as the heavy tech Nasdaq Composite finished a bit lower off 0.1%. Second quarter earnings season opens next week with several big banks and financial companies leading the results parade. Early expectations from economists and strategists are calling for modest increases across the board. The big news late Friday and early Saturday centered on bitcoin and the price level hovering in the $117,000 range, poised to move higher as demand strengthens.

President Trump on Monday seriously threatened Russia with heavy tariffs as high as 100%, frustrated and upset that Putin is ‘playing’ him with stepped-up warring, increased drone usage and targeting of civilian housing against Ukraine. Trump has now countered his views on supplying Ukraine with needed weapons and materials. He has given Putin 50 days to acknowledge a proposed ceasefire, with serious consequences. He also reiterated a 30% tariff, again to be levied against the European Union and Mexican products. Monday’s session was ‘lack-luster’ with all three indexes near flatline. Seth Merrill, chief investment officer at Crewe said; “Deep down, investors do believe that tariffs can have an inflationary impact. But until they see it show up in a n official government report they don’t feel like they have to act on it,” Investors and traders have taken a ‘laissez-faire’ attitude as the market doesn’t react as intently as when the first tariffs were announced.

Equities were pressured Tuesday as the CPI reported inflation crept up in June, 0.3% higher than May, at “2.7% year over year” according to government data. The 10 year Treasury note yield finished Tuesday at 4.5%. Big banks released quarterly earnings, with their stocks retreating slightly as results were not as ‘healthy’ as expected. Ongoing criticism by the President of Jerome Powell, the Fed chief, has now spilled over to the next selection candidate. Talk of firing has cooled as President Trump has signified that he will not fire Powell. Bitcoin was again the big news on the street as it hovered in the $116,000 range. With Trump’s positive endorsement of crypto currencies market interest has intensified. Stocks, like yesterday, were docile as many investors and traders were on the sideline. All three indexes perked up a bit in the afternoon with the S&P 500 edging back 0.1%, as the Dow Jones closed near flatline. The heavy tech Nasdaq lost 0.2%, a flat day indeed. Late Thursday saw the Nasdaq and S&P 500 hit record highs-again boosted by positive earnings reports from respected financial and tech companies and a general feeling that the economy is picking up steam.

Copper has been a strong performer, hovering at $5.55 a pound, with heavy speculation driving the metal since President Trump’s 50% tariff proposal. It has buoyed the metal, highlighting its integral importance in the many areas of usage; Electric Vehicles, computers, converters, electrical wiring and the manufacture of alloys of Brass and Bronze. The U.S. production is centered in three states, Arizona, New Mexico and Utah, with massive reserves in Michigan’s Upper Peninsula.

RUMBLINGS ON THE STREET

Abby Joseph Cohen, Professor of Business, Graduate School of Business, Columbia University, Barron’s – “The S&P 500 seems fully priced around 6300. If policy changes have negative consequences, the downside could be around 5800.”

Scott Black, Founder and President Delphi Management, Boston, Barron’s – “Powell has done a good job with monetary policy. TheFed’s balance sheet was $9 Trillion at the peak. He has wound it down to $6.7 Trillion.”

David Wagner, Portfolio manager at Aptus Capital Advisors, WSJ – We’ve been hitting new all time highs, yet there’s still continued skepticism. It feels like people are still very much on alert right now.”