April 29, 2026

This Pricing Window Is Short

Featured Read: Meta Reports Tonight

|

|

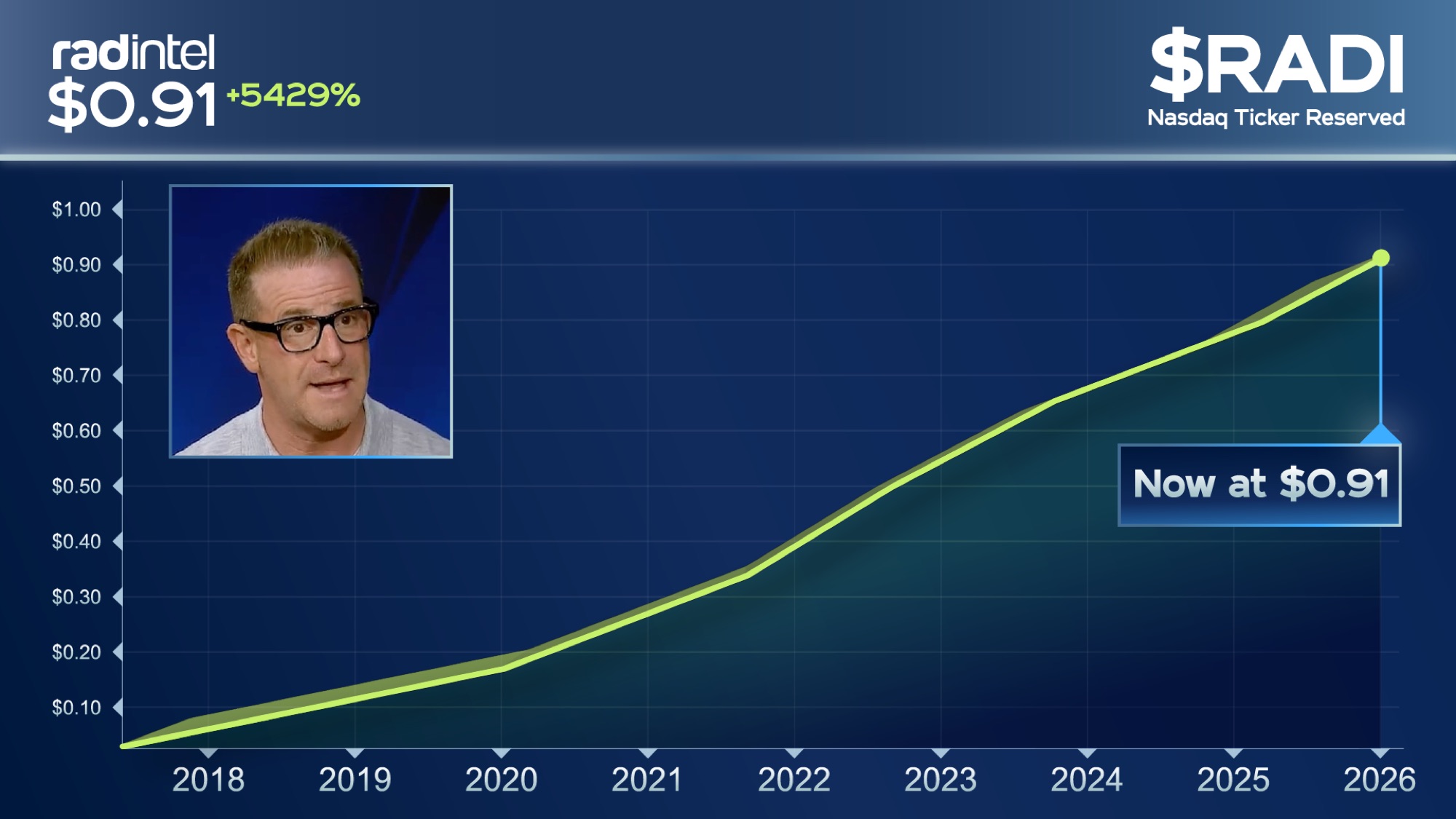

$RADI $0.91 ▲ |

Pricing Window Closing

Price Changes Tomorrow at 11:59pm PST. Invest at $0.91/Share.

RAD Intel’s current Reg A+ round remains open at $0.91 per share – though that price is scheduled to change. Final window at the current price ends April 30 at 11:59 PM PST.

|

|

|

| ► Invest Now at $0.91/Share |

20,000+ investors already in · $75M+ raised to date

Here’s What $0.91 Per Share Gets You

|

||

|

||

|

||

|

Backed by multiple institutional funds. Selected by the Adobe Design Fund. Supported by early operators from Google, Meta, YouTube, and Amazon.

|

$0.91 pricing window closes April 30 at 11:59 PM PST |

|

|

Lock In $0.91/Share Before the Price Changes. |

|

|

|

|

After tomorrow at 11:59 PM PST, this entry point is no longer available. |

FEATURED READ

META Reports Tonight.

Meta Platforms (NASDAQ: META) drops its Q1 2026 results after the close on April 29, and on paper the setup looks clean – a 14-quarter revenue beat streak, analyst consensus calling for $55.56 billion in revenue and $6.67 EPS, and a stock that just staged a 26.5% recovery off its March lows. Wall Street has 45 analysts at Strong Buy with a mean target of $854.

So why is this trade harder than it looks?

Because the number that actually moves this stock tonight isn’t revenue. It’s CapEx guidance.

Meta has committed $60 to $65 billion in AI infrastructure spending for 2026 – up from $69.69 billion across all of 2025, now potentially doubling. The company has locked in multi-year deals with Amazon AWS for Graviton5 chips, secured a fiber-optic supply agreement with Corning, and signed a 20-year nuclear power contract with Vistra. That infrastructure ambition is the story. Every forward word from Mark Zuckerberg on the call gets filtered through one question: does the ad engine justify the bill?

Here’s where it gets interesting. Q4 2025 operating margin already compressed 700 basis points year-over-year to 41%, and free cash flow fell 19% to $43.59 billion as long-term debt doubled to $58.7 billion. Analysts want Q2 guidance near $59.6 billion – roughly 25% year-over-year growth. Any capex step-up without a matching lift in revenue guidance could reprice the stock fast, especially after a 26.5% run into the print.

‘Please, Please, Please’: OpenAI CEO Sam Altman Begs Small Company for Help

As reported by Financial Times, those are the exact words OpenAI CEO Sam Altman spoke on an open line to a small company in Arapahoe County, Colorado… which now controls what could be the most important technology in the world. Altman is desperate to get his hands on it… and he’s not alone. This tech is now backed by Elon Musk, Jensen Huang, and more.

Click here to learn how you could invest in this breakthrough alongside Sam Altman and Elon Musk.

What the Options Market Is Pricing

Options traders are currently pricing approximately 14.66% implied move on the Q1 result – a wide band for a stock that has beaten revenue estimates in each of the past 14 quarters. The implied volatility heading into tonight reflects both the magnitude of expectations and the asymmetric risk in the capex narrative: beats are already partially priced; misses on margin or guidance are not.

Polymarket assigns a 93% probability Meta beats EPS, consistent with its track record. But this earnings season has been unforgiving even for beats – Netflix beat by 0.5% and dropped 9.7% post-print. Coursera aligned with estimates and fell 11.6%. A crowded long into a well-telegraphed beat is not the same thing as a safe long.

The Framework

Bull case: Revenue at or above $56.5 billion, ad growth near 30%, operating income on track to top 2025, and no upside capex surprise. Muse Spark – Meta’s latest AI model, released under Alexandr Wang’s Meta Superintelligence Labs – gets called out as a monetizable asset. Stock reclaims its 200-day SMA at $680 and runs toward analyst targets. A defined-risk bull structure – long call spread, May or June expiry, struck near the money – captures the move without full exposure to gap risk.

Bear case: Revenue below $53.5 billion, margin dips into the 30s, or 2026 capex guidance pushes materially above $65 billion with no offset. Ad growth below 20% would feed ROI skepticism heading into Q2. For traders expecting a sell-the-news reaction, a short-dated put spread captures the downside thesis with defined exposure. Reality Labs – which lost $19.2 billion in 2025 with similar losses guided for 2026 – remains the structural drag that never quite resolves.

Neutral/volatility case: A straddle or strangle struck near $675 captures movement regardless of direction, appropriate for traders who think the market reaction will be large but are uncertain of the vector. The 14.66% implied move sets the break-even zone.

Slight tangent, but it matters: Meta’s advertising exposure to the Iran conflict is a real but underappreciated wildcard. As oil surged past $110 a barrel in early April, advertisers in discretionary categories may have pulled back spend. Q1 results capture exactly that window. Management’s commentary on advertiser behavior in February and March could shift the narrative as much as the headline revenue number.

The pre-earnings setup is a stock priced for 30% ad growth to absorb a $115 billion spending year. Tonight’s print is the first data point that tells investors whether the math actually works.

Your Download Link Will Expire

If you still haven’t downloaded my free “Simple Options Trading For Beginners” guide…

…please take a few seconds and download it right now before your new temporary download link expires.

I eventually plan to charge money for this training, so do yourself a favor and download it now…

That way, no matter what it costs in the future, you’ll have a free copy on your computer.

Make sense?