April 30, 2026

The Reality of the $111 Billion Ceiling

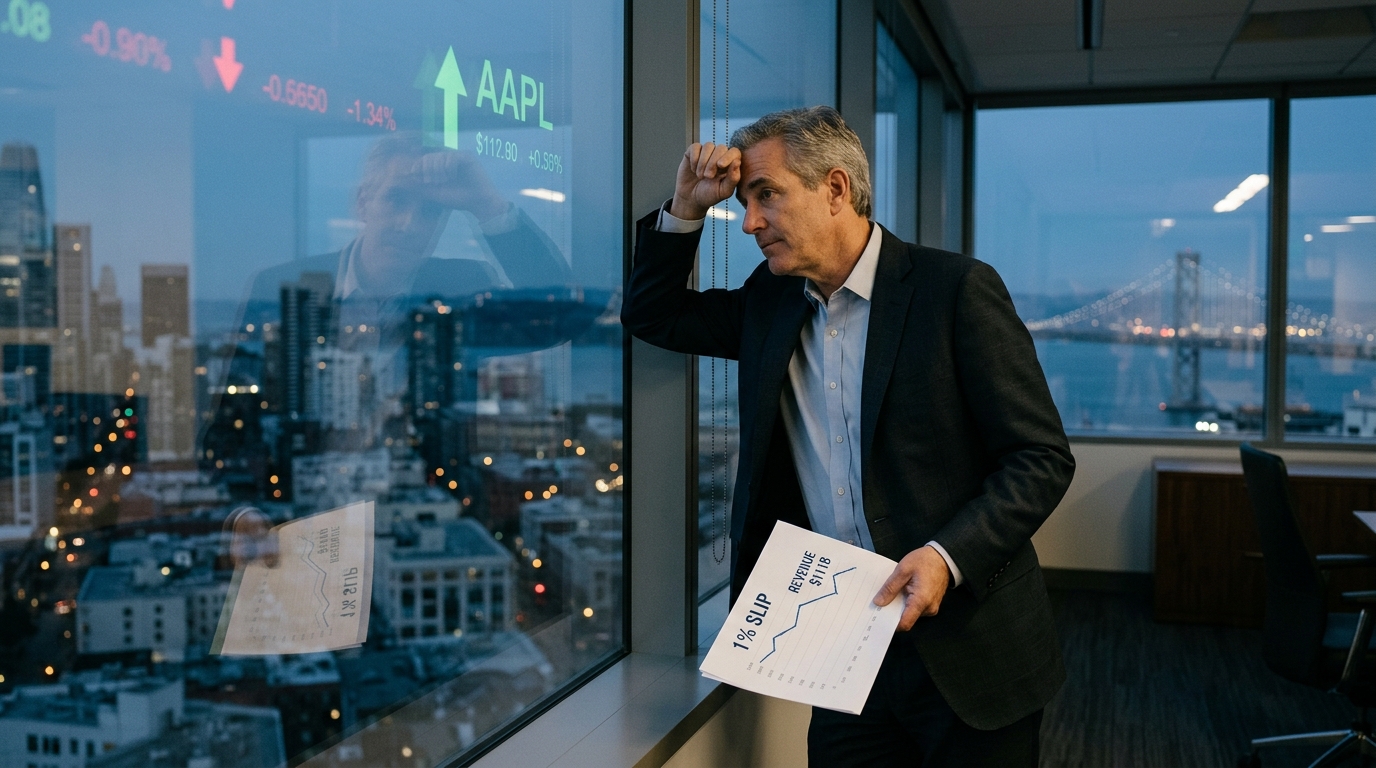

Apple beat everything. The stock barely moved. That’s the whole story.

Apple just posted the most profitable March quarter in its history and the stock slipped roughly half a percent after hours.

Revenue of $111.18 billion. EPS of $2.01 against a $1.95 consensus. Gross margin of 49.27%, nearly a full point ahead of estimates. Services at $30.98 billion, a new record, up 16% year over year. China up 28%. A $100 billion buyback authorization and a 4% dividend increase. Net income of $29.6 billion against a $28.5 billion expectation. June quarter guidance of 14% to 17% revenue growth, crushing the 9.5% analyst consensus by a mile.

The reaction? Barely anything.

Not because the numbers were bad. They weren’t. The issue is something harder to quantify — a slow shift in how the market thinks about Apple that has been building for two years. The company has become so large, so consistent, and so mechanically efficient at returning capital that it has stopped behaving like a growth stock. At $430 billion in trailing revenue, growing 15% means generating $65 billion in new revenue annually. That is larger than the total yearly revenue of most S&P 500 companies. The machine keeps running. The incremental excitement has to come from somewhere new. And right now, it isn’t obvious where that is.

This is what the law of large numbers looks like. Not a collapse. Not a miss. Just a ceiling.

Hidden in Tesla’s Filing: A $12 Billion “Super Startup”

Pull up Tesla’s most recent SEC filing. Page 5.

And you’ll see a single line showing $12 billion in revenue from a brand-new “super startup” Elon Musk has been quietly incubating inside Tesla.

This new “super startup” has nothing to do with cars or robots or space or AI…

But it sits at the center of what Blackstone calls “a $23 trillion investment opportunity.”

And on July 22, Elon is expected to pull back the curtain and reveal exactly what he’s building.

But Adam O’Dell already knows… and he reveals it all in this urgent video.

The $100 billion buyback is the tell. When a company cannot find a better use for capital at that scale, it gives the money back. Apple has done this brilliantly for over a decade. But compare it to what Amazon, Google, and Microsoft are doing right now — committing $100 billion or more into AI infrastructure, data centers, and model training. The market this earnings season has rewarded capacity bets over headline beats. Alphabet rallied nearly 10% on Google Cloud’s 63% growth and a $460 billion backlog. Apple, with cleaner numbers on almost every line, barely moved. That gap tells you exactly where growth expectations currently live.

There is also the margin compression coming. Memory costs are rising and Cook confirmed the impact will increase beyond the June quarter. Gross margin guidance for Q3 is 47.5% to 48.5%, down from 49.3% this quarter. Not a disaster, but a visible ceiling on near-term multiple expansion. And then there is the CEO transition — Tim Cook hands over to John Ternus on September 1, 2026. The first question Ternus will face is what Apple actually does with AI, and the Google Gemini partnership powering Siri is either a smart acceleration move or a quiet admission that Apple Intelligence is behind. Probably both.

When a fortress stops moving, the capital looking for motion goes somewhere else.

Right now two names are absorbing that displaced speculative interest in meaningfully different ways.

Allogene Therapeutics (ALLO) is a clinical-stage biotech developing off-the-shelf CAR T cell therapies — engineered from donor cells rather than a patient’s own, which addresses a core manufacturing bottleneck in existing CAR T platforms. The pivotal ALPHA3 trial posted interim data showing 58.3% MRD clearance in the treatment arm versus 16.7% in the observation arm, a 41.6% absolute difference that exceeded the clinically meaningful threshold of 25 to 30%. The company subsequently raised $200 million at $2.00 per share, extending its cash runway into Q1 2028. The next hard catalyst is proof-of-concept data from the RESOLUTION trial of ALLO-329 in autoimmune disease, expected June 2026. This is a binary risk profile — the kind that either works dramatically or doesn’t work at all. For traders who understand that asymmetry, the setup before a data read is a very specific kind of opportunity. Not for undiversified capital. But real.

GoDaddy (GDDY) is slower and less dramatic, but arguably more interesting on a risk-adjusted basis. Q1 2026 revenue came in at $1.3 billion, up 6%, at the high end of guidance. Normalized EBITDA of $414 million, up 13%, margin expanding 210 basis points to 33%. Free cash flow of $474 million, up 15%. Full-year 2026 FCF target of $1.8 billion. The AI integration is further along than most people realize — Aero AI Builder surpassed $10 million in annualized bookings within weeks of beta, and an internal AI sales agent is now handling thousands of calls and chats with what the company described as strong conversion. For 20 million small business customers globally, that kind of product-level AI embedding creates compounding retention leverage that shows up in margin before it shows up in revenue. The stock moved 4.7% on the quarter. It is not done moving.

Are 1 Billion iPhones About to Become Obsolete?

A secret Apple project may soon make today’s iPhones, Apple Watches, and iPads feel like relics. Behind this breakthrough is “Project Mulberry” – set to roll out across over a billion devices and disrupt a $9 trillion industry.

And one little-known company trading for less than $30, quietly supplies the critical chip behind it all. Early investors have a brief window before this goes mainstream.

Apple is not broken. The business is operating at arguably the highest quality level in its history. But there is a difference between a great business and a great stock at any given moment, and right now the market is slowly working through that distinction in real time.

For traders assessing AAPL from here: defined-risk bull structures in the $265 to $285 range reflect the buyback floor against June guidance upside. Collar strategies against existing long positions make sense given the margin compression risk into September. If the AI monetization story remains unresolved through the Ternus transition, a defined-risk bear spread targeting the $255 to $260 zone captures that overhang without unlimited downside.

The fortress is built. Cook built it as well as anyone could. The question is not whether Apple is a good company. It clearly is. The question is what happens to the capital that came for growth and is slowly realizing it signed up for a very expensive bond.

That capital moves. It already is. And the names it lands in — a binary biotech ahead of a June data read, a free cash flow compounder with AI margins nobody is modeling — are where the actual asymmetry lives right now.